March 12, 2026 | 9:30 AM EST

Martime and Freight Corridor Update

Conflict in the Middle East continues to disrupt regional and global supply chains. Since GCCA’s March 4 update, the operational picture has evolved from broad carrier suspensions to a more differentiated market: some carriers remain highly restrictive, while others are now reopening selected bookings using bonded land bridge and multimodal corridors to bypass the Strait of Hormuz.

The key issue for food and containerized trade is no longer only whether cargo can enter the region, but through which gateway, at what cost, and under what inland transport constraints.

Immediate and Medium-Term Supply Chain Disruption: Maritime

Suspension of Hormuz transits

Most major carriers have suspended transits through the Strait of Hormuz due to security and insurance risks. The closure is de facto rather than legal — insurers withdrawing coverage makes the route commercially unusable. Tanker and container ship traffic has fallen close to zero. Around 150+ vessels have anchored or delayed near the Gulf awaiting security clarity and those at anchor are at risk of attack.

Trans-Suez services suspended again

The resumption of Houthi rebel attacks on commercial shipping in the Red Sea has meant that most large container carriers have reinstated full diversion away from the Red Sea and Suez Canal, reversing tentative early-2026 returns. This means all/most traffic is rerouted around the Cape of Good Hope. This is a transit time extension of 10–15 days compared to Suez.

Affected Shipping Lanes Updates

- MSC remains the most legally aggressive major line. Its March 3 advisory declared an “End of Voyage” for all shipments under MSC custody destined for Arabian Gulf ports, with cargo to be discharged at the next safe port and placed at customers’ disposal. MSC also imposed a mandatory USD 800 per container surcharge, with onward transport requiring a new booking. MSC subsequently issued a similar End of Voyage declaration for certain exports from the Arabian and Persian Gulf.

- Maersk has not used MSC’s contract-termination approach, but its restrictions remain severe. As of March 9–11, Maersk was still suspending bookings across much of the Upper Gulf and maintaining restrictions on reefer, DG, OOG and most dry cargo for the UAE, Iraq, Kuwait, Qatar, Bahrain, parts of Saudi Arabia and parts of Oman, while keeping Jeddah, King Abdullah Port and Salalah open. Maersk has also suspended all vessel crossings through the Strait of Hormuz and earlier rerouted ME11 and MECL around the Cape of Good Hope. (Maersk March 9 Update, and March 11 vessels routes Situation Report )

- Hapag-Lloyd has suspended all vessel transits through the Strait of Hormuz until further notice, imposed a booking stop for UAE, Iraq, Kuwait, Qatar, Bahrain, Sohar, Dammam/Jubail and Yemen, and temporarily suspended its IG1 and KWF services while it evaluates safer revised port rotations. It has also published war-risk, contingency and emergency fuel surcharges. (Hapag-Lloyd ‘live ticker’)

- CMA CGM is the most important change since the March 4 GCCA note. After suspending bookings, reefer bookings and hazardous bookings in early March, CMA CGM announced on March 11 that it was reopening import bookings into Iraq, Kuwait, Qatar, Bahrain, Saudi Arabia and the UAE, and reopening export bookings from Iraq, Kuwait, Qatar, Bahrain, KSA and the UAE, using specifically designed multimodal solutions rather than normal Gulf port calls. Applicable cargo for these reopened flows is dry, frozen and in-gauge.

- ONE publicly announced a temporary suspension of new bookings to and from the Persian Gulf on March 2. In the sources reviewed here, I did not find a newer public advisory confirming a broad reopening, so the prudent working assumption is that ONE remains cautious and exception-led rather than fully normalized.

Insurance and Risk Environment

There have been no substantial changes since GCCA’s March 4th update. Shifts in insurances positions are not anticipated, until/unless there is a discernible indication of a de-escalation or cessation of hostilities in the Persian Gulf (Global Cold Chain Alliance)

System-Level Effects

The system-level effect is shifting from simple vessel delay to network redesign. GCCA identified Salalah, Sohar, Duqm and Khor Fakkan as fallback gateways; that remains broadly correct, but the market has now moved one step further, with carriers and forwarders actively building sea-road and sea-road-feeder solutions off those gateways.

For cold chain operators, the principal operational risks remain:

- Diversion-port congestion

- Container dwell time growth

- Reefer plug scarcity

- Inland truck availability and border clearance timing

- …and a widening cost gap between normal maritime delivery and contingency routing.

Land Bridge Alternative Routes for Food and Container Goods (in detail)

Land alternatives are now the most dynamic part of the market. (See an update from GCCA member RSA Global on how it is working with customers on contingency routes for reefer cargo, as well as updates from global freight forwarder DHL here and CMA CGM here.) Sohar and Salalah in Oman, Khorfakkan and Fujairah in the UAE, and Jeddah in Saudi Arabia are functioning as key entry points, supported by bonded transit and simplified customs processes across the GCC.

- Jeddah corridor (Red Sea to GCC)

Carriers are standing up capacity on the freight route from Port of Jeddah to connect onward — via feeder vessels or trucking — to Dammam, Iraq, Kuwait, Qatar, Bahrain, and the UAE. Europe–Egypt–Saudi–GCC multimodal routing options remain operational. . This is currently the clearest large-scale alternative for food and container goods coming from Europe, the Mediterranean and transiting Asia-Europe networks that can discharge on the Red Seaside. - Oman corridors (Salalah and Sohar)

Oman is now functioning as the main non-Hormuz maritime workaround.Majorfreight forwarders report Sohar and Salalah are fully operational, and that bonded trucking from those ports into GCC markets is active. CMA CGM is using Sohar both for imports into the Gulf and for exports out of the Gulf, including movements from Kuwait, Qatar, Bahrain, and Iraq via feeder plus land bridge. For food and frozen cargo, these Oman corridors are especially important because they provide the most credible non-Hormuz maritime interface still tied into GCC road networks. - UAE east-coast bypass: Khor Fakkan / Fujairah to Jebel Ali / Khalifa

A practical UAE alternative isemerging. Leading regional operators report that cargo blocked from the Arabian Gulf is being rerouted through Khorfakkan, Sohar, and Jeddah, with onward distribution by truck. It also notes DP World is offering bonded truck service from Khor Fakkan and Fujairah to Jebel Ali. Carriers are standing up bonded land bridge options from Khor Fakkan, Fujairah or Sohar to Khalifa and Jebel Ali for local UAE cargo and for onward feedering into Upper Gulf markets. This is probably the most important short-term route for UAE-bound containerised and food cargo that can tolerate one inland transfer. - Qatar via Saudi land border using TIR

Qatar has moved beyond contingency planning into formal facilitation. On 7 March, Qatar Chamber, working with the General Authority of Customs, called on operators to use the TIR system for fast-track movement of goods across the Saudi land border, supported by the Al-Nadeebelectronic customs system. This is a strong indicator that Qatar is working to “institutionalize” permanent overland supply routes, particularly for food and consumer goods. - Iraq alternatives: Aqaba, Mersinand southern/northern land bridges

CMA CGM’s reopened export solutions are especially notable for Iraq. It lists an Aqaba corridor for South Iraq origins and a Mersin corridor for North Iraq origins, alongside Jeddah and Sohar options. That suggests a widening map of land-bridge alternatives for containerised cargo out of Iraq, including refrigerated and frozen cargo where equipment and border procedures allow.

Constraints on Land Bridge Routes

These land-bridge solutions are real, but they are not substitutes for unconstrained maritime access.

- First, they are capacity-limited. GCCA has warned that fallback ports were not designed to absorb full diversion volumes, and all carriers and forwarders are warning that congestion and longer inland transit times are likely as more vessels divert.

- Second, they are cargo-selective. CMA CGM’s reopened solutions apply to dry, frozen and in-gauge cargo, not a blanket reopening of all cargo classes. Maersk and Hapag-Lloyd remain much more restrictive on reefer, DG, and certain Gulf destinations. (CMA CGM)

- Third, they are cost additive. MSC’s USD 800/container deviation charge, Maersk’s emergency freight increases, Hapag-Lloyd’s war-risk/contingency/emergency fuel surcharges, and CMA CGM’s emergency conflict and fuel surcharges all indicate that the land bridge is being layered on top of a high-cost risk environment, not replacing it. (MSC)

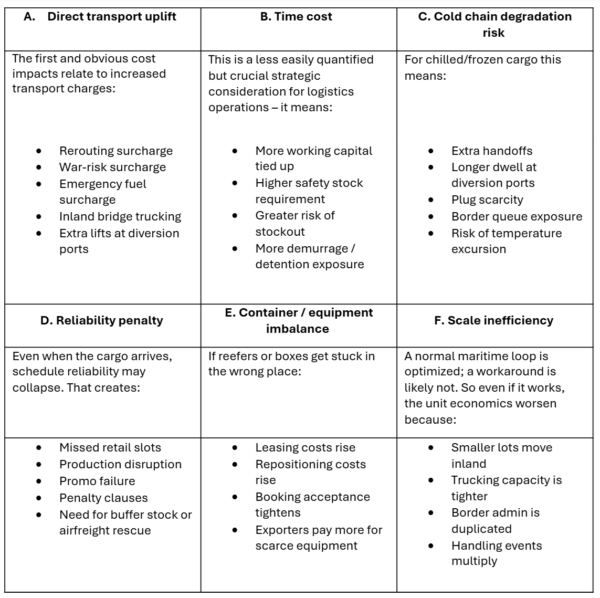

Cost Modelling for Supply Chain Route Diversions

Normal route cost versus Disrupted route cost

As businesses explore alternatives to traditional maritime routings, including land bridge options, to keep goods moving across the GCC Region, they will encounter a range of cost and operational pressures.

The crucial thing to bear in mind in mapping the likely cost impact of a disruption like this is that it is a dynamic situation with constantly changing variables. The primary cost driver will be the duration of the crisis — as more logistics companies shift to alternative land routes, bottlenecks will emerge, transshipment hubs will face capacity strain, and competition for vehicles, drivers, and fuel will intensify, affecting both cost and reliability. The pattern will be uneven as multiple actors react, and there is the risk of military action-related changes (like drone attacks on ships at anchor.)

Updated Disruption Projections

First-order impacts (Immediate)

The likely immediate picture is continued growth in diversions to Jeddah, Salalah, Sohar, Khor Fakkan and Fujairah, with more cargo transferring from sea to bonded road haulage. Food and frozen cargo should move, but with higher inland coordination demands and likely premium pricing. (DHL)

Second-order impacts (2–4 weeks)

The main risk is that today’s workaround becomes tomorrow’s bottleneck: queueing at diversion ports, customs and border friction, reefer power constraints, truck repositioning shortages, and slower container returns. GCCA’s earlier warning on reefer equipment imbalance remains highly relevant if substantial empty equipment gets trapped in disrupted Gulf loops while export hubs in Asia tighten.

Medium-term impacts (One month and beyond)

If disruption persists, the market is likely to settle into a two-tier model: a smaller set of direct maritime services into safe gateways, plus a structurally larger role for multimodal GCC land bridges. That would be operationally workable for many dry and frozen food flows, but more expensive, more documentation-heavy, and more vulnerable to inland capacity shocks than the pre-crisis maritime model.

For additional information, contact Shane Brennan, Senior Vice President, Global Policy, Projects & Partnerships: sbrennan@gcca.org

Published Date

March 12, 2026

Topic

Advocacy, Commodity Storage & Handling, Energy, Food Loss & Waste, Government & Regulatory Affairs, Insurance & Risk Management, International, Legal Issues, Supply Chain Operations, Transportation & Logistics

Region

Africa, Asia-Pacific, Australia, Canada, Central & South America, Europe, Mexico, United States

Sector

GCCA Transportation, GCCA Warehouse, Global Cold Chain Foundation