March 9, 2026 | 9:00 AM EST

Energy Market Impact

Overview

The conflict with Iran is causing oil and shipping disruption, this is already having an impact on energy prices, stock and currency markets around the world. Below, GCCA sets out the likely impact on cold chain operations around the world. It makes a comparison to the shock experienced in 2022, following the Russian invasion of Ukraine.

Cold Chain Logistics Exposure

Energy often represents 30-50% of operating costs in cold chain logistics. This makes the sector highly sensitive to energy price volatility.

Cold chain operations are energy intensive in three main areas.

- Diesel fuel for refrigerated transport (road and maritime)

- Electricity for warehousing operations

- Electricity and natural gas for freezing and (in some cases) food processing activities

Today v. Ukraine Invasion 2022

While this crisis shares similarities with the 2022 Ukraine invasion, there are key differences, particularly in how the economic impact will be distributed regionally. The 2022 crisis was largely centered on Russian gas supplies, with Europe bearing the brunt. This crisis has broader global reach.

As roughly 20% of global oil and LNG trade passes through the Strait of Hormuz, sustained disruption is likely to drive a significant energy price spike, affecting:

- Diesel and marine fuel

- Electricity for refrigeration

- Natural gas used in food processing

Unlike 2022, oil prices could be hit just as hard. However, gas and electricity shocks, while probably less severe, are likely to spread more widely across the globe. Energy price spikes may also reduce consumer confidence and food demand, creating secondary impacts for the food supply chain.

For all impact analysis, the crucial dependency is how long the conflict and paralysis of oil and LNG exports from the region lasts.

Expected Energy Price Behavior

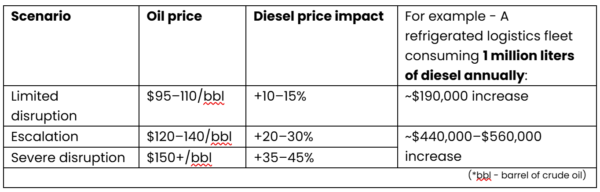

Oil and Transport Fuel

Oil markets respond rapidly to geopolitical shocks. Transport costs therefore rise first and most visibly.

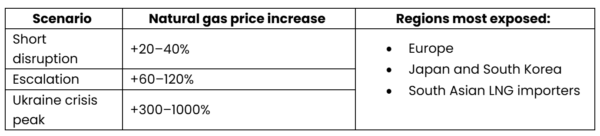

Natural Gas and LNG markets

The natural gas shock would likely be less severe than in 2022. The previous crisis resulted from the collapse of pipeline supplies from Russia to Europe. An Iran conflict would instead affect LNG shipping routes, particularly exports from Qatar. Expected natural gas price changes:

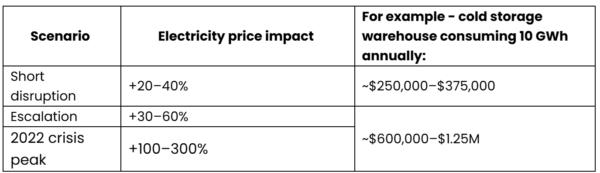

Electricity Prices

Electricity is a major cost driver for refrigerated warehouses and food processing. In many markets, notably Europe and the UK, natural gas-fired power plants determine marginal electricity prices.

Regional Breakdown

Africa

- Africa is vulnerable to oil price shocks due to dependence on imported fuels and diesel-powered transport.

- Rising diesel costs will increase trucking, food distribution, and energy expenses, especially where grid reliability is low.

- This energy-driven food inflation will lessen consumer purchasing power, shifting demand to cheaper staples and cutting consumption of chilled products.

China

China has strong policy tools to stabilize energy prices. Authorities can:

- Adjust electricity tariffs

- Increase coal generation

- Use strategic oil reserves

These mechanisms help limit domestic price spikes.

Europe

Europe remains the region most sensitive to electricity price increases because natural gas often sets wholesale power prices. Potential impacts include:

- Higher cold storage electricity costs

- Increased food processing costs

- Margin pressure for refrigerated logistics

The European Commission may support industry through electricity subsidies or market interventions.

North America

- North America is relatively insulated due to large domestic oil and natural gas production.

- Electricity price increases are likely to be smaller than in Europe or Asia.

- Transport fuel costs will still rise due to globally determined oil prices.

Northeast Asia

- Japan and South Korea rely heavily on imported LNG.

- If shipping through Hormuz is disrupted, electricity costs could increase significantly.

- Governments may intervene through LNG procurement coordination and electricity subsidies.

Oceania (Australia and New Zealand)

- Oceania is likely to see moderate impacts, primarily through global oil markets.

- Higher diesel prices could increase the cost of long-distance refrigerated trucking and food exports, particularly for shipments to Asian markets.

- Electricity impacts are likely to be smaller due to diversified power systems, although higher fuel prices could still raise logistics costs across export supply chains.

South and Southeast Asia

- Countries such as India, Bangladesh, and Indonesia already subsidize fuel and electricity.

- Energy price increases could significantly increase logistics costs, although fiscal constraints may limit long-term government support.

South America

- South America is partly insulated due to significant hydropower generation and regional oil production.

- Electricity price increases may therefore be more limited than in Europe or Asia. However, higher global oil prices would still increase diesel costs.

- Major food exporters will face higher shipping and cold chain transport costs.

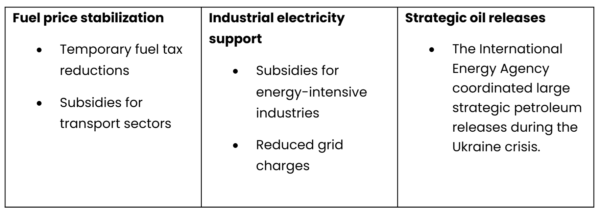

Government Policy Responses

Governments now have a clearer policy playbook following the 2022 crisis. Similar measures could be used again. However, fiscal constraints mean support will likely be more targeted than in 2022. Possible interventions include:

Consumer Confidence and Food Purchasing Behavior

Energy price spikes will drive economy wide inflation, with knock-on implications. Consumer sentiment and food purchasing patterns may create additional pressure on the cold chain sector, and with this reduced consumer confidence, higher fuel and energy bills also reduce disposable income.

During the 2022 energy crisis, consumer confidence declined significantly across many economies.

Consumers typically respond by:

- Reducing discretionary spending

- Purchasing lower-cost food options

- Minimizing food waste

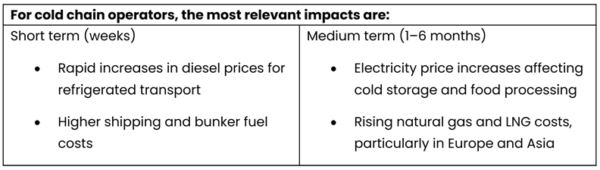

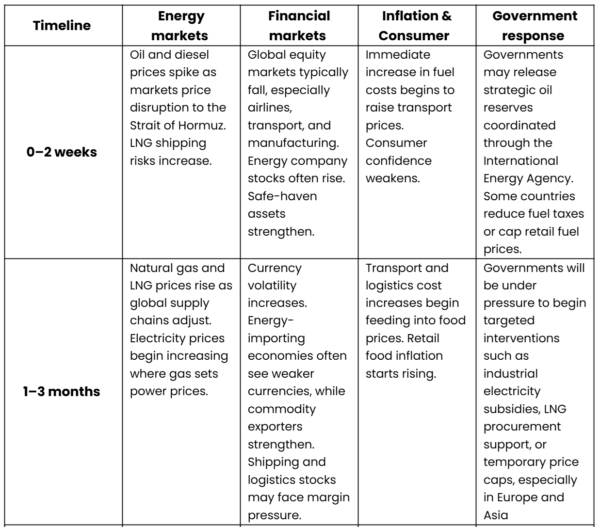

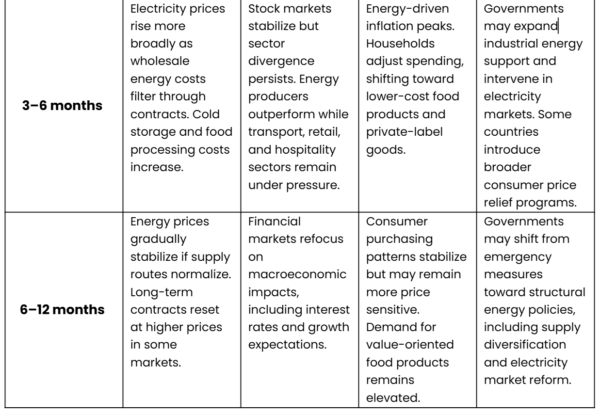

Timeline of Impacts (Projected)

Published Date

March 9, 2026

Topic

Advocacy, Cold Chain Development, Energy, Food Loss & Waste, Government & Regulatory Affairs, International, Supply Chain Operations, Sustainability, Transportation & Logistics

Region

Africa, Asia-Pacific, Australia, Canada, Central & South America, Europe, Mexico, United States

Sector

GCCA Transportation, GCCA Warehouse, Global Cold Chain Foundation